The Italian aviation market boiled last week with the announcement, in less than 24 hours, that both Ryanair and Wizz Air, the famous ultra low-costs, would be opening their very own bases in Venice’s Marco Polo airport, for the next Summer season.

Though both carriers had a small presence in the airport, connecting the capital of Veneto region to some of its most important bases, this is the first time each that any of the two will base aircraft in the terminal.

This is important because it will allow the airlines to widely expand the array of destinations and frequencies locally – and they really went for it.

Ryanair will launch 18 new routes, adding up to the six that were already existent, basing three aircraft in Marco Polo Airport. This will make, the company says, for more than 160 weekly departures and 100 new direct job positions.

The airline, that added a base in Treviso (which is 40 minutes away from Venice, and is sold as Venice/Treviso) last Summer, also announced two new services from Verona, which is also in Veneto region.

Of the new routes from Venice’s Marco Polo terminal, two domestic connections, to Cagliari and Trapani, will be relocated from Treviso.

«The announcement of today of 86 routes [next Summer season], 20 [of these] new, shows Ryanair’s capacity of being at the forefront on supporting the rebound of Italian tourism», said Jason McGuinness, Ryanair’s Commercial Director, in a press release.

Meanwhile, Wizz Air will add 16 routes to Venice, that will add to the 10 it already operates; according to the airline, this will lead to the creation of 70 new jobs.

In Ryanair’s press release, Camillo Bozzolo, Commercial Director for the Aviation part of Gruppo SAVE, which manages Veneto’s largest airport, stated in Ryanair’s press release that «for Gruppo SAVE, [Ryanair’s new base] represents the confirmation that [our] airports are central in the airlines’ developement strategies».

The battle for dominance is only starting

Indeed, Veneto should be central in airlines’ further growth in Italy as a market with plenty of potential. With a population of almost five million, it has the fourth largest GDP of the country and is an tourism powerhouse.

This way, it would only be natural that Ryanair, by far the largest carrier in the country, and Wizz, which is investing heavily in Italy since COVID started, would want a share of this very market. That, however, would come only with the help of SAVE, since the company runs the four major airports of the region, in Brescia (which only receives cargo operations), Treviso, Venice and Verona.

And in the position of airlines with the lowest cost base in Europe, Wizz and especially Ryanair are very well-known for their no-bullshit approach to negotiations with airports, not afraid to ask for heavily discounted prices and leveraging on their market power to get good deals with the terminal operators.

So while these carriers cannot just bypass SAVE to serve the Veneto market by going to another airport nearby, SAVE cannot just refuse these airlines’ business since they can heavily stimulate demand by slashing prices. So a solution that worked for both parties must have been found, and the opening of the Treviso base earlier this Summer had already indicated this trend.

However, it’s not all happiness and profits as these ULCCs land in Venice; while Italy has been a good performer this previous season and the market has immense potential, there is a problem: already two stabilished ULCCs run large operations from Venice.

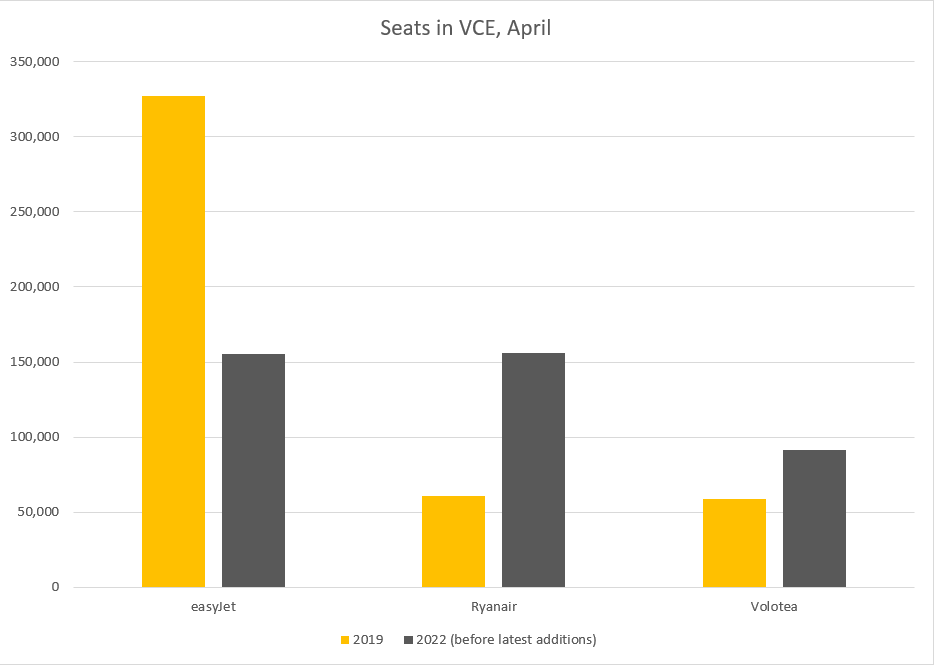

According to data gathered by Aviacionline with Cirium’s Diio Mi application, Volotea and easyJet respectively owned 27.5%, by far the largest, and 4.9% of all seats offered in Venice on April 2019. While Volotea was the third by number of seats – after Ryanair, by the way -, the Spanish carrier had 467 flights offered versus Ryanair’s 322; it’s just that, at that point in time, Volotea’s fleet consisted mostly of a considerably smaller aircraft, the Boeing 717.

Flash forward to April 2022 – before both Wizz and Ryanair even loaded their new flights. Ryanair was already the leader by number of seats in Venice (15.4%), followed closely by easyJet (15.3%) and Volotea, which now operates a full Airbus fleet and has considerably more flights, with 9.1% of the seats in Venice.

Remark: Wizz did not have most of their Eastern Europe connections loaded into Cirium’s system, albeit they were for sale; paralelly, Ryanair’s Vienna connection was the only of the new flights that already appeared in the system. In any case, we ignored these flaws as we considered they did not distort, representatively, the overall picture.

Now we start to see a pattern here: easyJet’s position in the Venice market is one that’s way more defensive than any of its low-cost competitors’, shrinking all the way in a key base. But this is not an isolated case at Venice: throughought Italy, easyJet has been a slow mover during COVID.

Bottom line: Venice is an important base easyJet had already shrank considerably from April 2019 to April 2022, whereas most airlines in Italy have tried to rebound fast, as this is a very important market where they have already a loyal customer base.

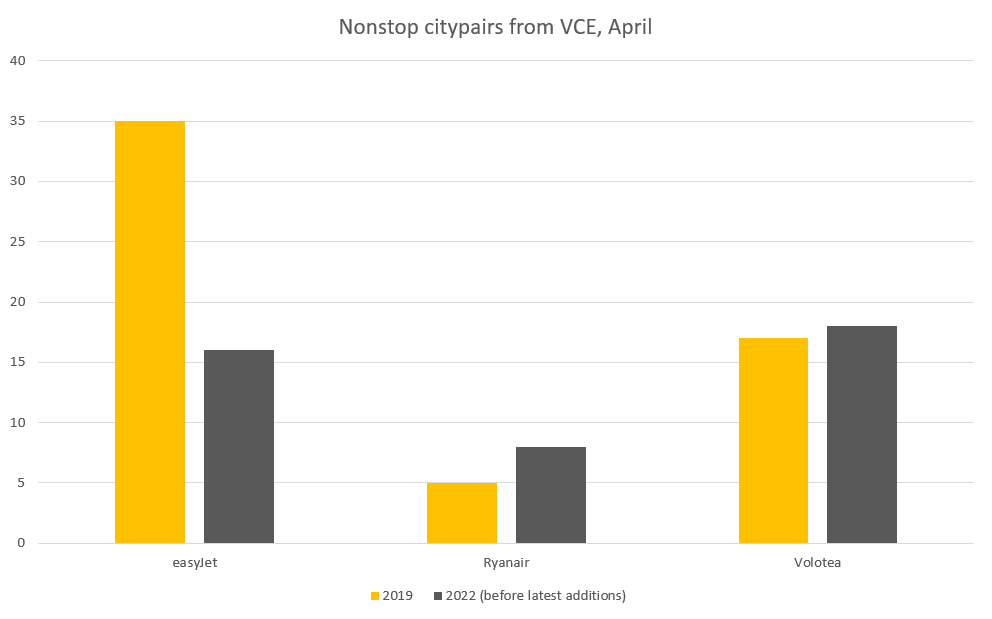

In terms of citypairs, the reductions were also massive, but most surprisingly, Volotea came out as provisional leader in direct connections from Venice. With Ryanair’s and Wizz’s new flights, the airline will quickly fall behind, though.

As you can see in the graphs, from 2019 to 2022 easyJet did not recover as quick in terms of destinations either. But «opportunity knocks», as they say, and while easyJet was deep sleeping, Ryanair and Wizz went for it.

Routes: what are Ryanair and Wizz up to?

But seeing there’s a void is not enough; to better understand the airline’s strategies upon this incursion into the Venice market, let’s take a deeper look at the destinations announced both by Ryanair and Wizz Air.

Ryanair has announced 18 new routes from its new base in Venice/Marco Polo. Of these, in April 2022:

- Nine were not operated by anybody on April 2019 and will count with no competition – Comiso, Cork, Crotone, Gdansk, Katowice, Nuremberg, Odessa, Santander and Trapani;

- Two were operated by at least one player on April 2019 but will count with no competition – Menorca and Stockholm;

- Seven will count with competition from the off – Cagliari, Helsinki, Lisbon, Madrid, Marseille, Toulouse and Vienna.

Of these seven routes, only in three – Cagliari, Marseille and Toulouse – Ryanair will go face-to-face with either easyJet or Volotea. On the other ones the airline will be competing with network carriers, which fundamentally cater to a different passenger since they don’t have the habit of flooding the market with capacity, then «trashing» it, as I’ve heard from a source one of these days, with insanely low fares.

While Ryanair and Wizz can do this and make a profit, network carriers simply cannot.

Therefore, only in 16.6% of the routes – representing only 9.8% of its expected capacity by ASKs, Ryanair will face true competition. Cagliari will also see competition by Wizz Air, as it is an important domestic connection.

Meanwhile, at Wizz, of the 14 new routes – excluding the two that will be launched way after April – will face competition like this:

- Seven were not operated by anybody on April 2019 and will count with no competition – Fuerteventura, Lamezia Terme, Mykonos, Palma de Mallorca, Prague, Reykjavik and Tallinn;

- One was operated by at least one player on April 2019 but will count with no competition – Lampedusa;

- Six will count with competition from the off – Cagliari, Casablanca, London/Luton, Naples, Tel Aviv and Thira.

Once again, filtering out the legacy carrier – El Al to Tel Aviv – we have that the other five routes will face competition of the ULCCs. Wizz’s ASK data at Cirium is still not available.

Bottom Line: who will win going forward?

All in all: while both low-costs are not completely avoiding competition, their strategy is simple: to fill in the gaps they perceived as left – or unserved – by easyJet in what is one of the most important markets for the British company in Italy.

Now the only remaining strongholds of the company in the country will be Milan/Malpensa, a higher-cost airport which other ULCCs long avoided, and Naples – albeit the airline is still shrunk there, and Ryanair has already outlined aggressive growth plans there going forward.

Paralelly, thankfully to Volotea – whose business model is simple: to replicate the ULCC model, but avoiding competition by connecting thinner routes – this means that none of its routes where it has a monopoly from Venice within ULCCs will be affected. That is Athens, Brindisi, Bilbao, Hannover, Luxembourg and Thira.

But whether there is competition or whether is not, getting those routes to work – and to work quick – is apparently seen as of utmost importance for both Ryanair and Wizz.

Both, in their press releases, have announced flights from their bases will be operated by their most efficient aircraft; the 737 MAX 8200, in the case of Ryanair, and the A321neo, in the case of Wizz. Although they can excel in the market through the «trashing» strategy, to make it work will only happen if they keep costs down.

But both players are prepared to whatever comes next: asked by Aviacionline during the World Routes 2021 event if he was ready for a fare war with Wizz Air in the Italian market, Ryanair’s Commercial Director Jason McGuinness said «we would need to increase our fares».

The calm waters of Venice will definitely get hot next Summer.