Last morning’s announcement that Düsseldorf’s Eurowings will be joining forces, in select routes, with Spanish ultra low-cost carrier (ULCC) Volotea, raised some eyebrows in the industry — albeit at a highly speculative level, still.

Both airlines, in a joint press release, were clear to say that this is strictly a «sales partnership» — more specifically a Memorandum of Understanding towards that goal –, whereby Volotea will sell «more than 100» of Eurowings’ routes in its channels, with the German airline selling «around 40» of Volotea’s in its own.

Corriere della Sera’s aviation journalist Leonard Berberi, however, noted that in the presentation of the new partnership «there is a glimpse that in the past few months the parts have also worked into something else».

Indeed, Eurowings — and its iterations — have always been the underperformers of the Lufthansa Group, its parent company. In the last quarter with available financial data, the group reported an EBIT margin for Eurowings, excluding equity investment earnings, that stood at around 5.8%, while the group had a margin of 10.1%.

That quarter tends to be the strongest of Europe’s short-haul business, where Eurowings is focused on (note the Eurowings Discover spinoff is reported as a part of Lufthansa, not Eurowings).

Corriere reported that Eurowing’s average cost per seat is at around EUR100, while Volotea’s average cost is at EUR59. That difference, say analysts heard by the Italian newspaper, «could bring the Lufthansa Group to consider a merger» with the Spanish ULCC.

Increasing Eurowings’ footprint outside its core markets, particularly outisde German cities, is another consideration that took the Düsseldorf carrier to make its first step, according to the press release.

«Step by step, we are strengthening the ‘Euro’ in our Eurowings brand name», stated Jens Bischof, Eurowings’ CEO. «Our roots are in Germany, but we are becoming more and more a European airline. Having established Eurowings in Northern and Eastern Europe with recent base openings in Prague and Stockholm, our next step is to expand booking options towards Southern Europe.»

«The mutual sales cooperation envisaged with Volotea would allow us to offer our customers many new and exciting destinations in France and Italy as well as enhanced connectivity within Southern Europe.»

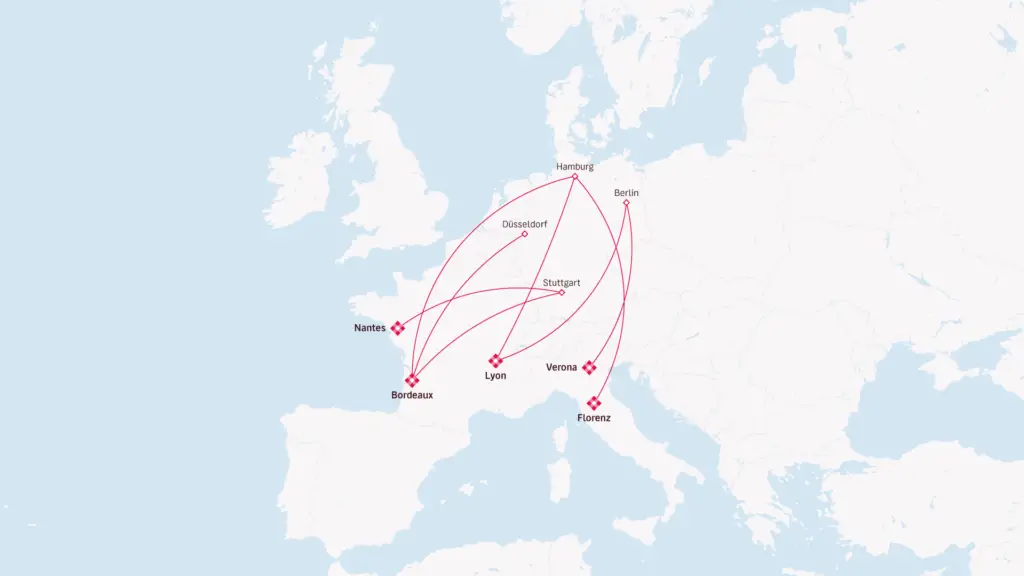

Apart from an already-existing base in Hamburg (where it exclusively served a contract with Airbus), Volotea has 18 operational bases; Eurowings, in turn, has 12. These figures refer to the next Summer season.

Besides the absence of overlap between both airlines’ networks, which would give both access to very important markets, there is the fleet similarity.

While the pandemic brought air travel to a halt in 2020, Volotea took the opportunity to end its fleet transition, retiring the 13 remaining Boeing 717s it had in its fleet and bringing a new lot of Airbus A320s.

Having ended 2019 with a fleet of 13 717 and 19 A319s, according to Planespotters.net, the Spanish ULCC ended 2022 with 20 A319s and 21 A320s — which conveniently is the same aircraft type used by Eurowings. The German airline currently operates almost 80 aircraft of the family.

As Carlos Muñoz, Volotea’s CEO, stated in the joint press release, «the planned strategic agreement with Eurowings is significant and unique […] and signals the potential for a stronger, long-term partnership.»

However, while Volotea could be an interesting target for the German airline group to develop actual low-cost travel within its system, this currently stands as a highly speculative hypothesis.