Who is filling the gap after Ryanair «quits» Athens for Winter

/https://aviacionlinecdn.eleco.com.ar/media/2022/10/12-scaled.jpg)

Here is a fact that is older than time: Ryanair does not like when things don’t go their way, especially when dealing with suppliers — whether it is aircraft manufacturers, governments or airport operators.

In Greece, this was no different as, in early September, Europe’s largest airline group said, in a press release to the local market, that they would be dropping out from its Athens base for the Winter. In typical Ryanair fashion, the airline claimed Athens would be «losing more than $200 million of investment in Athens airport, a vital gateway for the Greek economy».

The airline claimed that two factors put the country out of favour with the Irish group; Germany’s «monopoly group» Fraport, who «[offered] no incentive to stimulate traffic during the winter season», and the Greek government, who «does not provide long-term incentives for airlines to invest in Athens airport during off-peak periods or to develop tourism in the way that Spain, Italy, Portugal and Cyprus have done».

Fraport does not run Athens Airport (the government is the majority shareholder), but it does run 14 regional airports in Greece.

«At a time when other governments and airports are reducing fees and introducing tourism recovery programs», the press release adds, «the Greek government continues to apply an airport development fee of €12 per passenger, making Greek access fees uncompetitive.»

And it finished: «it is inexplicable that the Greek government does not use incentives at Greek airports to promote Greek businesses and jobs but instead protects German practices with high cost charges».

Yes, indeed, the rife between Ryanair and Fraport has been going for a while — at the start of this year, they announced the closure of all their operations in Frankfurt-Main Airport, citing the increase in airport charges.

But Ryanair’s loss is someone else’s gain — especially in the case of Greece, where the country has two major home carriers.

The situation in Greece’s aviation market

Besides being a beautiful country with enormous touristic appeal, Greece has a large outbound market, with a population of over 10 million people, of which over a million live in the islands, which makes air transport particularly attractive.

As such, the country counts three major, «local» airlines. First, and perhaps the most known of them, Aegean Airlines, which operates a fleet of the Airbus A320 family aircraft. The airline, which is a member of Star Alliance, also owns Olympic Air, a turboprop operator — the «successor» of the flag-carrier Olympic Airlines that focuses on domestic routes.

Lastly, Sky Express, which for years retained a small fleet of turboprops, took the pandemic to grow rapidly and to incorporate jets; now, according to Planespotters.net, it operates a fleet of eight Airbus A320neos, one A320ceo, eight ATR 72 and four ATR 42.

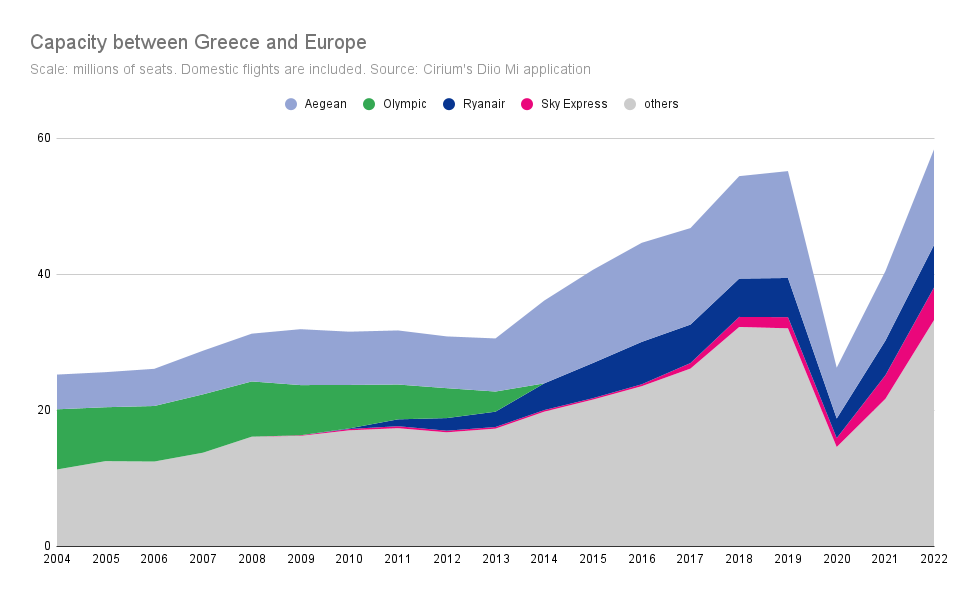

With that being said, while the hometown carriers have grown over the years, they fell in importance when compared to foreign airlines. This can be observed on the graph below, with data obtained with the help of Cirium’s Diio Mi application.

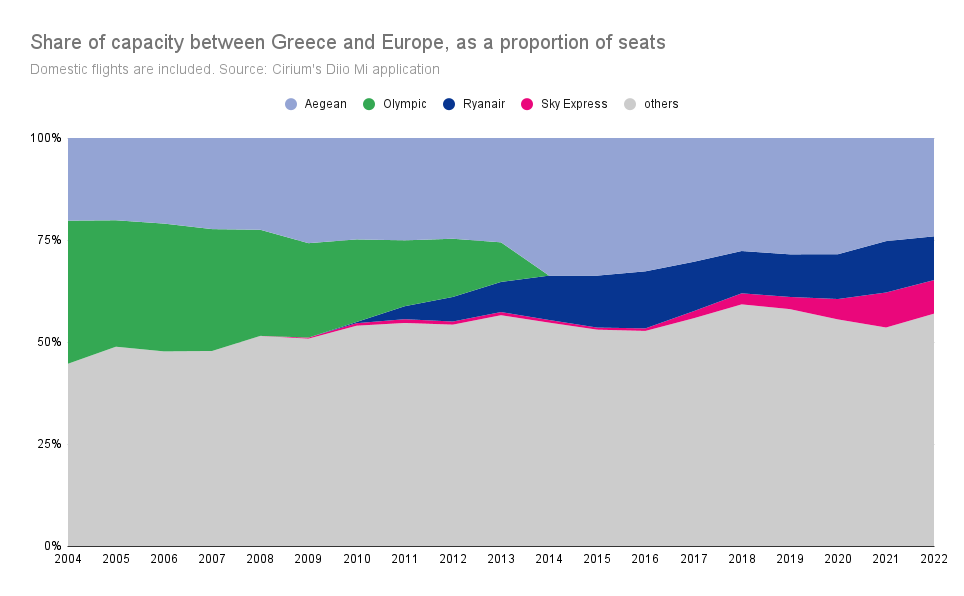

Or, when putting it in a percentage perspective, that trend is clearer (after 2013, Aegean and Olympic are counted as a single entity).

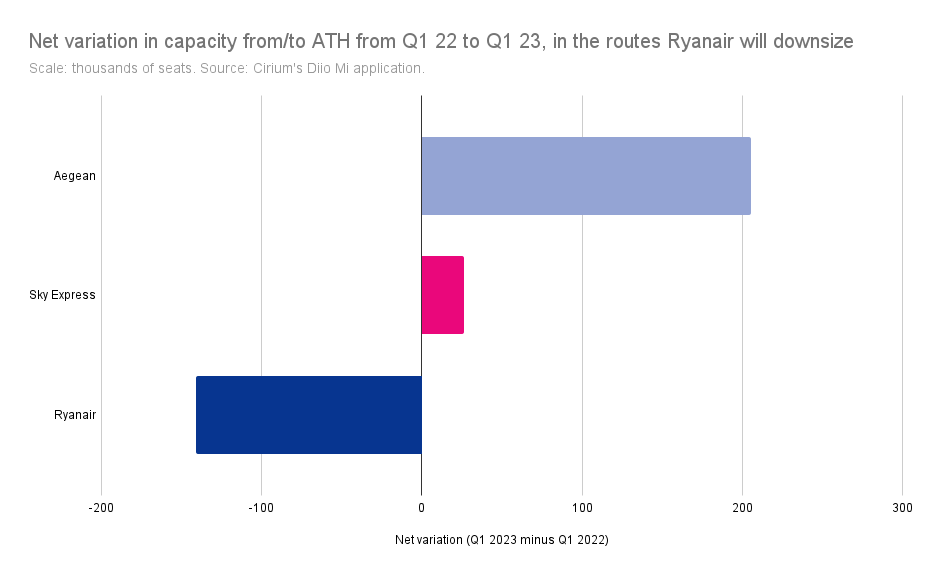

Still, the Greek carriers are very important in assuring a connectivity to and from the country. In 2022, Aegean alone, by far the country’s largest airline, is selling 14 million seats (to European countries, Greece included), while Sky Express is selling 4.8 million, closing the cap to Ryanair, which is selling 6.25 million seats.

As such, Ryanair, for the Winter season, is dropping numerous routes. For the first quarter of 2023, according to Cirium, the group will offer just over 221 thousand seats to and from Athens, a drop of 36% in comparison with the same period in 2022.

There will be no new routes by the Irish airline to the airport in the aforementioned period of 2023, largely because of that. Meanwhile, ten will be slashed and four will be reduced.

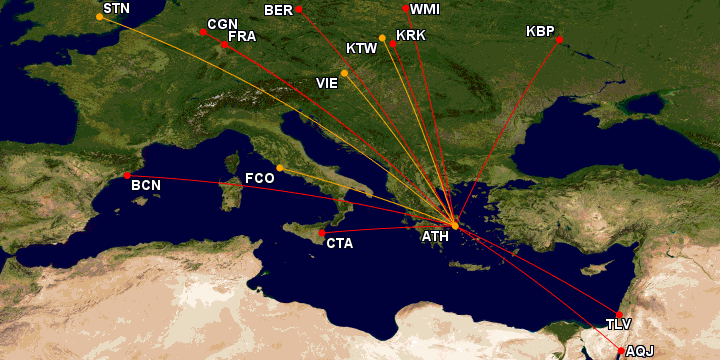

The map below shows, in red, Ryanair’s routes from Athens that won’t be back for the first quarter of 2023, while the routes in orange see a significant reduction in capacity (Katowice will see a 7% reduction, while the others will see a cutback of over 19%).

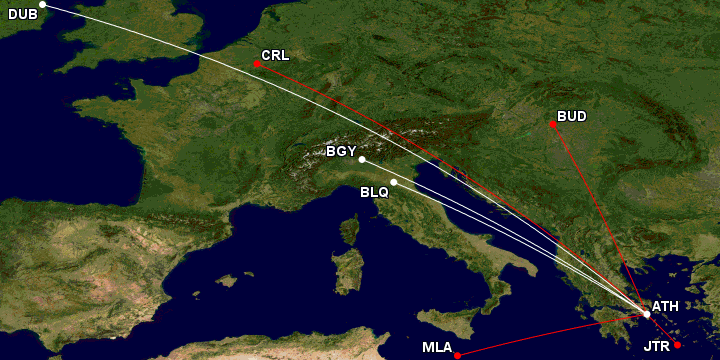

The remaining network for the first quarter of 2023 (below) will be barebones when compared to the previous diversity of routes during a relatively weak quarter. In this map, the routes in red will see an increase in capacity versus the same period in 2022, while the ones in white will not grow significantly.

Naturally, the network tends to grow significantly from one quarter to the next as Summer approaches and demand grows — it would be foolish to think that Ryanair would ignore this demand. How the Summer season will be is still largely unknown, for the Irish LCC still hasn’t loaded its schedules on Cirium’s Diio Mi application.

But what is at stake here really is the Winter capacity (since, at annoucing the closure of the Athens base «for the Winter season» Ryanair implied Athens would be kept as a seasonal base). In other words, keep traffic to and from Greece going even out of the peak season.

This interview to a Greek TV station with the CEO of Ryanair DAC — the Irish airline of the Ryanair group –, Eddie Wilson, just after the closure of the Winter base in Athens, is very didactic in what the company means by that. It’s not only about airport fees, but also for passenger fees levied by the national government, which charges EUR12 per passenger, regardless of the season.

«I can understand they [the Greek government] don’t want to [lower the tax] for the Summer because everybody wants to come to Greece in the Summer», said the executive.

Still, whether or not the Greek government bites Ryanair’s bait — as this is an old tactic for the group –, one thing is a fact: the company will not base aircraft in the country for this Winter season.

And which airlines will benefit from that?

Who will gain from Ryanair’s retreat

Data from Cirium for the first quarter of 2023 shows that, in the ten routes Ryanair dropped, three will not see a replacement; the ones to Kiev (for obvious reasons), to Aqaba (Jordan) and Catania (Italy).

The other seven that were slashed from the airline’s schedule versus the same period will all see replacements (below).

| Destination | Who grows | Notes |

|---|---|---|

| BCN | Aegean grows ~30%; Vueling grows ~60% | |

| BER | Aegean doubles capacity | easyJet and Scoot dropped the route |

| CGN | Aegean starts its Summer flights way earlier than last year | Arguably there might be some overlap with DUS, which Aegean and Eurowings serve year-round |

| FRA | Aegean and Lufthansa increase ~20% each | Slot congestion arguably hampers further growth |

| KRK | No replacement through most of the quarter, but Aegean starts flights by late March | |

| TLV | Israir (same capacity); Aegean doubles its presence; Bluebird Airways and TUS Airways enter the route; Arkia and El Al grow | |

| WMI | Aegean more than doubles | Aegean operates from WAW |

With these swaps, of the seven destinations, from Athens, that will see service from other airlines, four will have recovered its capacity (by number of seats) already in the first quarter of 2022: Barcelona (an increase of 32.2% versus the same period in 2022), Frankfurt (9.7%), Tel Aviv (over 100%, as Bluebird underreported the number of seats) and Warsaw (WAW and WMI; 29.5%).

Meanwhile, in the destinations from where Ryanair reduced its capacity, competitors are also looking at increasing their positions — chart below.

| Destination | Who grows | Notes |

|---|---|---|

| FCO | Aegean grows ~60%, ITA doubles, Sky Express grows ~85% | |

| KTW | Wizz adds a year-round operation | Ryanair decreases only 7% in this route |

| STN | Jet2 starts year-round operation, to LHR Aegean grows ~33%, BA grows ~17% and Sky Express ~85%. To LGW easyJet increases ~83%, Wizz more than doubles capacity and finally, to Luton, Wizz increases ~83%. | London's capacity limitations may deny carriers (especially in LHR and LGW) from further growth |

| VIE | Aegean increases by ~48%, Austrian by ~60%. | Wizz also drops from this market |

Overall, one airline leaves as a clear winner from this: Aegean. In short, as far as the routes Ryanair will downsize, Aegean’s growth will more than cover the difference left by Ryanair.

The airline, even though holding the advantage of being the hometown carrier, is not an obvious substitute to Ryanair. After all, its costs are much higher than the Irish airline’s.

Financial data from the second quarter of this year, in fact, shows that the CASK — the cost for flying one ASK — for the Greek airline was 7.38 cents of euro. Meanwhile, Ryanair’s was at 3.74 cents of euro, in other words, the cost base of Aegean is double of Ryanair’s.

Aegean does manage to more than reconcile this difference by charging higher fares — by Aviacionline’s estimations, EUR91.8 for Aegean’s versus Ryanair’s EUR34.7.

But at the same time, the high cost base means that engaging in price wars with the Irish group is much more difficult for Aegean, which is why that is a fantastic opportunity for the Greek airline to embrace this opportunity.

And what about Sky Express?

Sky Express has been raising eyebrows in the Greek market since it started its A320 expansion in 2020. Not for nothing, since during the pandemic the company started a neck-breaking expansion; in 2021, its capacity was more than double what it had seen in 2019, and in 2022, it grew a further 38% by number of seats, according to Cirium’s Diio Mi application.

With that, the airline is growing even more for the first quarter of 2023 with respect to the same period in 2022, but at a slower pace.

While the airline is private and thus its financial disclosures are very limited, the more likely hypothesis is that the airline, from now on, will try to focus on securing a loyal customer base — and thus a profitable operation — in the already existing routes.

This does not mean, however, that there will be no new routes; for the first quarter of 2023, Sky Express will be flying from Athens to Milan/Malpensa (competing with Aegean, easyJet, Wizz Air and, via Bergamo, Ryanair), Munich (competing with Aegean and Lufthansa) and Sofia (competing with Aegean and Bulgaria Air).

These routes were not on schedule for the same period in 2022 and may also hint that the airline does have the appetite to put up a fight in already crowded markets.

But there is a trend in this process; while Ryanair left Greece because it thought there would be better places to funnel its investments (especially ones that tax passengers less), the local carriers may just have the assets to fill in the void, or at least to keep the expansion going, despite the EUR12 fee imposed on passengers to and from Greece.

While naturally airlines — and passengers — would be better off without that fee, or with lower airport fees charged by the airport operators, Sky Express and especially Aegean are very optimistic about the future of air travel in Greece, according to their network planning. And while they may not produce unit costs at the level of the ultra low-cost carriers, they know that market well.

After all, Aegean does manage to command a premium for its tickets with respect to the ULCCs, according to its financial statements. Costs might be higher, but so are their fares.

And whatever the results of Ryanair’s move of leaving the Athens winter base are, there will be far-reaching consequences in the Greek market for the seasons to come; apparently, the local carriers will be more than happy to cover what has been left behind.

Para comentar, debés estar registradoPor favor, iniciá sesión