How is the Italy-US market shaping up post-COVID?

/https://aviacionlinecdn.eleco.com.ar/media/2021/11/United_Airlines_Boeing_777-200ER_N78008_landing_at_Milan_Malpensa_Airport.jpg)

Ah, beautiful Italy; it’s no wonder why millions of Americans flocked here every year before COVID, and therefore no wonder why airlines are perpetually crazy for this market, trying to profit on that love.

Conversely, Italo-Americans are a large community in the States, which makes demand from the other side also very strong year round – and this is not to mention Italians’ love for America.

Naturally, as a long-haul air bridge, this is a market that suffered a lot with the consequences of the pandemic, and the subsequent travel restrictions and uncertainty. And a lot has happened since 2019; Air Italy and Alitalia went bust.

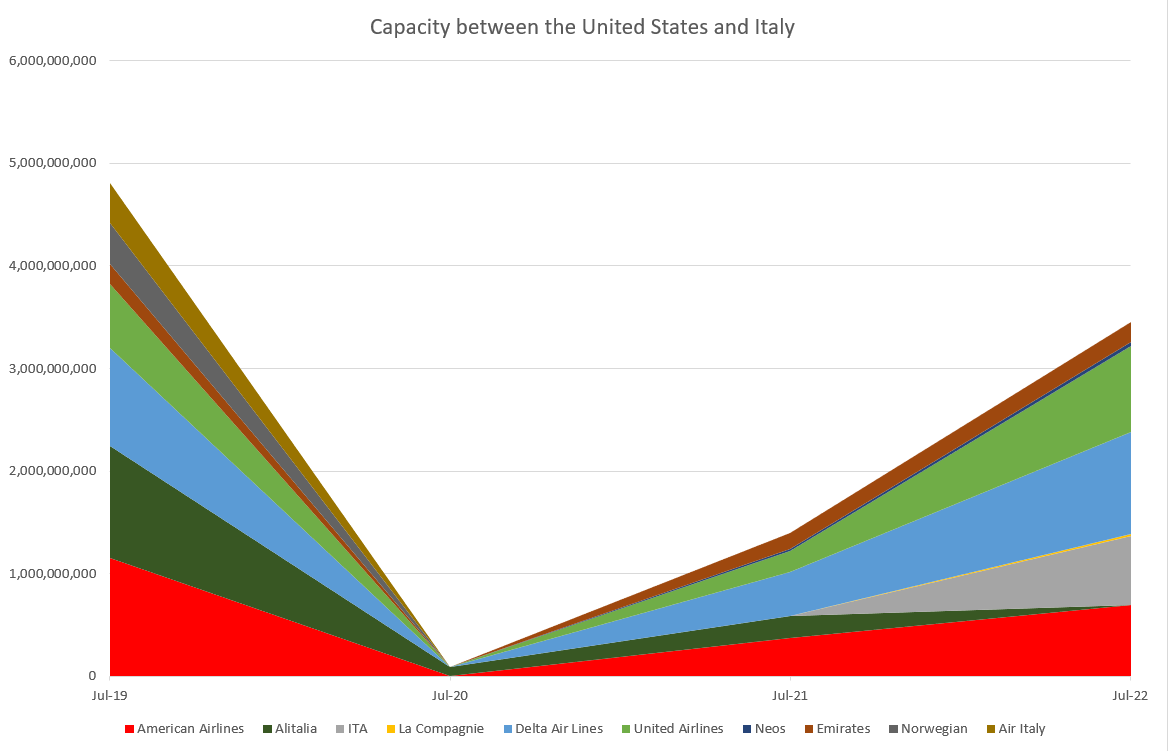

So the question arises – how is this market shaping up post-COVID? Aviacionline will help answer this question looking at the comparison between the schedules of July in the years of 2018, 2019, 2020, 2021 and 2022 with the help of Cirium’s Diio Mi application.

2019

Pre-COVID, the Italy-US market was so interesting for airlines that even Alitalia managed to earn money in a bunch of these routes. According to a report gathered by Corriere della Sera, in 2018 the airline actually turned a profit in the Rome-Los Angeles and Rome-New York legs, also more or less breaking even in the Rome-Boston route.

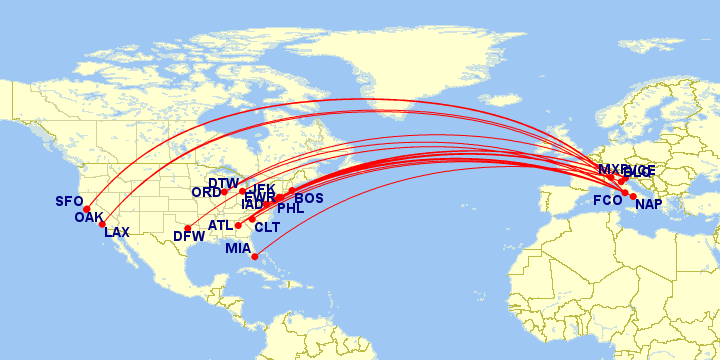

But overall, this is an absolutely diverse market, full of different routes not only to the gateways, as you can see.

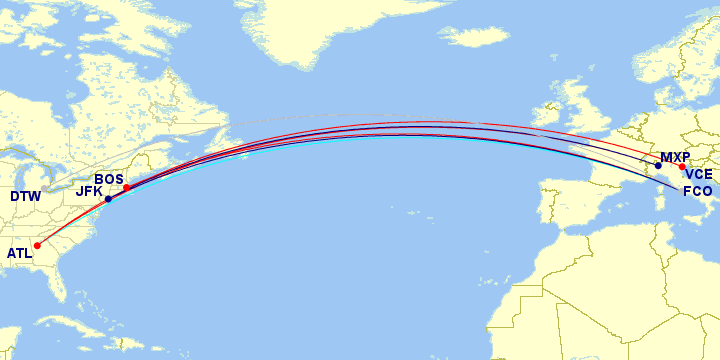

In July 2019, seven different airlines operated passenger services between both countries: Air Italy, American Airlines, Alitalia, Delta Air Lines, Emirates, Norwegian Air Shuttle and United Airlines.

In said month, these seven airlines sold 2,409 flights, 646,627 seats and 4.8 billion ASKs between Italy and the United States and vice-versa.

Now this market is full of nuances. Alitalia naturally focused on connecting its major hub, Fiumicino, to the US’ major cities: Boston, Chicago, Los Angeles, Miami, New York and Washington. Last but not least, New York was also connected to Milan, a very premium-centered connection.

Not for nothing, Italy’s flag carrier was in the second position in terms of ASK capacity between both countries.

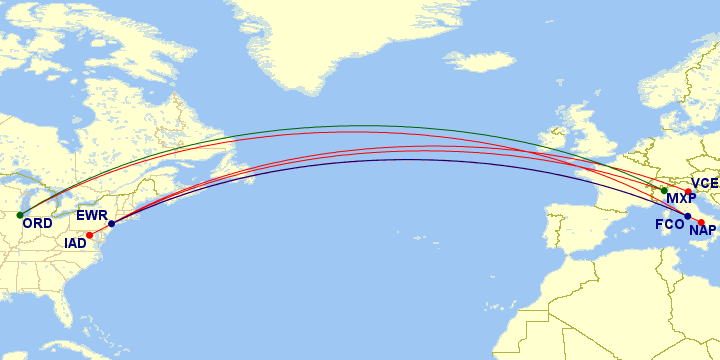

Meanwhile, the US3 – American, Delta and United – expectedly connected their main hubs in Center-Western US to Milan and Rome.

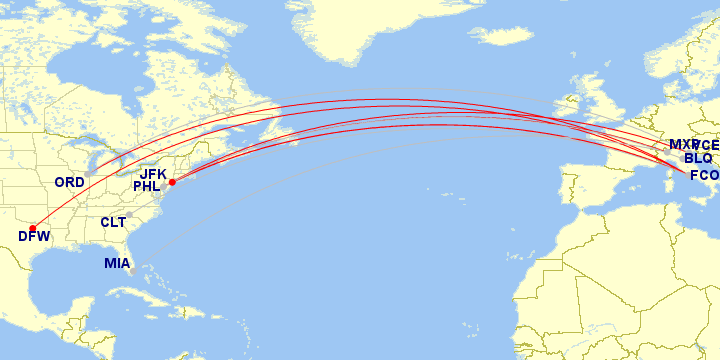

There were a few exceptions to this rule, however; American Airlines connected its Philadelphia hub to Bologna, and United Airlines flew between Newark and Naples. Meanwhile, Venice was the only secondary city served by the three carriers; American from Chicago and Philadelphia, Delta from Atlanta and New York and United from Newark.

Besides these four carriers, the three remaining were definitely as interesting in the context of the Italian market; let’s discuss them one by one.

First, the most famous case, Emirates. The UAE carrier did a daily run from Milan to New York, operated by the Airbus A380.

In fact, this specific fifth-freedom route raised the fury of the US3, who were disgusted with a foreign carrier they claimed to be subsidized creating an unfair competition position.

This gets us to the second carrier of this bunch, Air Italy. Until a couple of years before, they were called Meridiana and operated just a bunch of flights from Naples and Palermo to New York.

Now, they had grown to own 8.1% of the market by ASKs, connecting Milan to Los Angeles, Miami, New York and even San Francisco.

Because the airline was now 49% owned by Qatar Airways, the US3 frequently said that Air Italy was just a proxy puppeted by the Middle Eastern carrier to further advance into the profitable Europe-US market.

And last but not least, we had Norwegian Air Shuttle in its ultimately failed low-cost, long-haul venture. The airline deployed its 787 in four routes to the US from Rome/Fiumicino: Boston, Los Angeles, New York and Oakland (in the San Francisco area).

So there you have it: a very diverse set of airlines connecting the two countries with all sorts of products for all sorts of likings. Little did the industry imagine how the next year would have been.

In total, July 2019 saw 2,409 flights, 4.8 billion ASKs and 646,627 seats offered from the United States to Italy and vice-versa.

2020

As you may remember, Italy was the first epicenter of COVID-19 in the Western world. This reflected, logically, in the travel between both, with tourism effectively banned from the two sides.

Therefore, in July 2020 only two routes were active: Rome-Boston and Rome-New York with Alitalia.

The disastrous numbers translated into mere 50 flights, 12,500 seats sold and 84.9 million ASKs – down over 95% from a year before.

2021

Now July 2021 saw a little rebound versus the previous year. This is because US travellers were again welcomed into Europe.

This meant that the three US majors were back in this game, with Alitalia offering basically the same it offered in 2020 – it’s just that the Boston frequency was shifted to strenghten the JFK operation instead.

The biggest losers here were the West Coast of the United States and the secondary cities in Italy; of these, only Venice remained, with 15 runs to JFK operated by Delta.

Obviously the network became much more restricted to the hubs not only because of the reduced traffic, but because the airlines wanted to preserve their dominance position where they were already strong in order to stimulate demand.

With this, operations like Philadelphia-Bologna becomes unnecessary for American Airlines, if they can do Philadelphia-London-Bologna in partnership with British Airways. Filling airplanes is easier by strenghtening its own hubs and its own partner’s hubs.

And as far as airlines go, all that survived COVID had returned to this important transatlantic market. Air Italy went bust in February 2020 and Norwegian withdrew from long-haul flying with the pandemic, so these were the only casualties.

At the same time, a new entrant decided to try its luck with the returning American tourists; Neos, a large charter airline in Italy, started a Milan-New York route.

Overall, though, July 2021 saw 716 flights from Italy to the US and vice-versa, with 199,979 seats for sale and almost 1.4 billion ASKs – still miles behind the 4.8 billion of 2019, but way ahead the terrible number of the same month in 2020.

2022

This is shaping up to be the first year of relative normalcy, with the US reopening its borders to vaccinated travelers, and this translates into more generous schedules from the airlines’ side.

All in all, the US-Italy market in July 2022 will have over 3.4 billion ASKs in capacity, with 1,888 flights and 476,458 seats sold.

ITA, the Italian state’s startup, designed to replace Alitalia, has enough capacity to put it in fourth place, behind of the US majors and very close to the third, American Airlines. Alitalia now holds 19.7% of the capacity, by ASKs, between both countries.

Another route that surprisingly remains is the Milan-New York – one that, in Alitalia years, lost money, but one that ITA, with its new, leaner structure, expects to make money at.

As far as flights to secondary cities in Italy, Venice has pretty much recovered its previous network – only Chicago is missing -, while Naples’ run to Newark is back. Bologna, however, is still not in the plans of the airlines.

And in terms of airlines, the Italy-US market will remain with seven players. While Air Italy went bust and Norwegian withdrew from long-haul, Neos is selling its Milan-New York for the next Summer season – in fact, it is keeping this route through the Winter – and France’s La Compagnie is expected to start flights between Malpensa and Newark with its full-Business aircraft.

The Milan-New York market, therefore, will have pretty much recovered to 2019 capacity numbers, then; however, with seven simultaneous players instead of 2019’s six.

This is a premium-heavy market whose flight, before the pandemic, Emirates’ CEO Sir Tim Clark said «[was] completely full all the time” and «we should have two [flights] on there, but I can’t get the slots into JFK» in an interview to The Points Guy.

The talking point from now on will be: will all these airlines run such flights profitably? Only time will tell.

But the two winners from the pandemic in this market are undoubtedly two: Delta and United. These two not only have the capacity from 2019 restored, but have also more capacity for July 2022 than pre-pandemic between the US and Italy.

In 2019, Delta was a close third, behind American and Alitalia, in capacity between the US and Italy. Now, the airline will leap to a comfortable first position, offering 993.9 million ASKs, versus 955.6 million in July 2019.

While the double daily flight from Atlanta to Rome passed to a daily frequency only and the Detroit-Rome route will not return, this will be more than compensated, with, along with some aircraft upgauges, the routes from New York/JFK to Milan and Rome going from one daily in July 2019 to two daily in July 2022.

But the airline making the most progress from 2019 to 2022 is United, that will jump from a distant fourth place in 2019 (618.4 million ASKs) to a comfortable second in 2022 (836.7 million ASKs).

Besides maintaining services to all routes it operated that Summer, it will increase frequencies from daily to double daily in the Newark-Rome run and start a Chicago-Milan operation.

This is a stark difference to American Airlines, which will lose the lead in capacity, falling from 1.155 billion ASKs between the two countries in July 2019 to 692.1 million ASKs in July 2022.

None of the routes operated by AA will see any increase in capacity, and four will not return: Charlotte-Rome, Miami-Milan, Chicago-Venice and Philadelphia-Bologna. So from 10 daily flights in some days of July 2019, the airline will operate six in July 2022, versus United’s eight (it was six in 2019) and Delta’s nine (eight in 2019).

However airlines think demand will behave in the upcoming Summer season, the battle is on. And as those months get closer and airlines – especially the ones that are traded in the stock exchange – disclose their sales observations, we will have a better picture of such an important market.

The cards, though, are already on the table, and these seven players could not hope more for their hands to be the winner.

Para comentar, debés estar registradoPor favor, iniciá sesión