What is Air Europa’s strategy for its «Express» subsidiary?

/https://aviacionlinecdn.eleco.com.ar/media/2023/10/Frankfurt_Airport_Aeronova_Air_Europa_Express_Boeing_737-8GPWL_EC-NUZ_DSC00634.jpg)

A known tactic of established European airlines to lower their costs is to launch subsidiaries, in an attempt at making this business unit deliver superior margins.

At IAG — the owner of British Airways and Iberia –, Vueling operates as a separate entity, delivering a low-cost product in bases across Western Europe, while Iberia Express was launched more than 10 years ago, more closely tied to Iberia and pressuring the latter to restructure.

Still in Spain, Globalia’s Air Europa has attempted a similar approach. The current rendition of Air Europa Express was founded in 2016 as an attempt at, in Globalia’s own words, «the reduction of the costs of crew and the enhancement of efficiency and consumption of long haul [sic] flights.»

Air Europa Express’ scope was that of regional flights at the time, incorporating the group’s ATR and Embraer fleets, which naturally come with higher unit costs vis-à-vis the mainline Boeing 737-800 operations.

Halfway last year, however, the airline started introducing 737-800 in its fleet, parallel to the phase-out of the regional aircraft. It had already been started in 2019, but the two aircraft were returned to mainline Air Europa as the COVID-19 pandemic hit.

Currently, Air Europa Express only operates the 737-800. One airline is fully integrated to the other, thus providing important feed to Air Europa’s network, including the long-haul operation.

More crucially, Air Europa Express can provide better margins by having lower labor costs versus the main airline, while benefitting from the same pricing/distribution/revenue structure of the main airline.

As with other airlines in the continent, this is not something the employees of the Air Europa have taken lightly. The fourth collective agreement with the airline’s pilots, last amended in 2021, provides that Air Europa Express could replace its Embraer fleet, of which there were eleven, by jets with a maximum of 189 seats, a clear reference to the 737-800.

Air Europa Express’ growth, however, would be limited to a maximum of 18 aircraft. This was conditioned that Air Europa’s fleet would grow by one aircraft for every two Air Europa Express added after a 13 aircraft threshold (the ATRs were not included in the limitations).

As such, as the fleet of Embraer 195 was phased out, the group was able to begin adding the Boeing 737 to the lower-cost operation. This growth was more expressive this Summer season; Air Europa Express now operates eight 737-800, according to Planespotters.net.

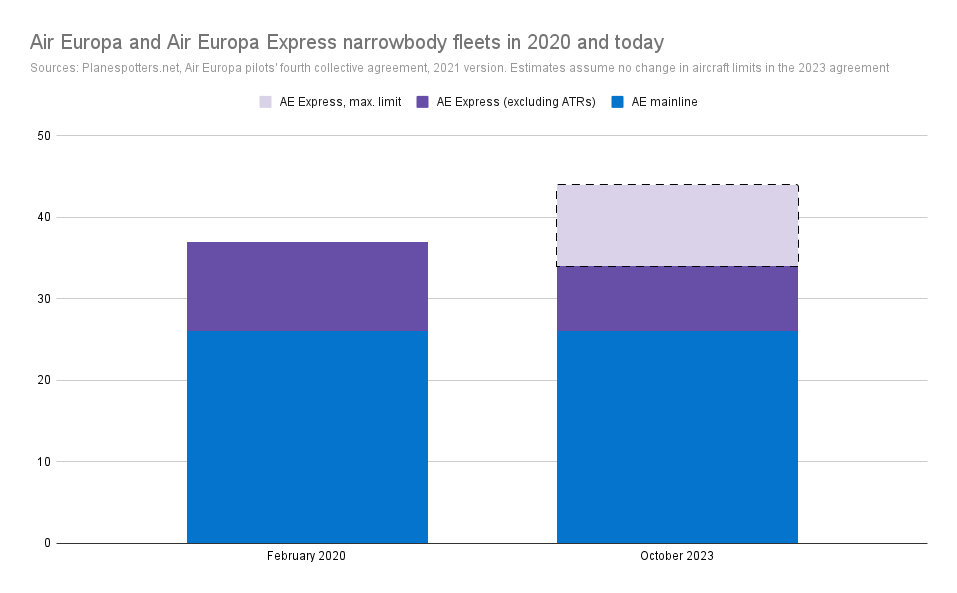

The graph below depicts the group’s narrowbody fleet in 2020, before the phase out of the Embraer 195 started, and today. The picture also projects Air Europa Express’ 18 aircraft «limit». Reaching this threshold would imply that mainline Air Europa would have to add another three aircraft, as per the collective agreement.

This projection assumes that in the newest collective pre-agreement of Air Europa’s mainline pilots, no concessions in this regard were made. Spanish pilots union SEPLA stated in a press release that the deal was reached «without giving in the fundamental rights acquired in the fourth agreement».

Air Europa Express would thus have another ten aircraft in its allowance, although mainline Air Europa would have to add three.

Of note, this is not a pure exchange from mainline to Express; the pilots’ agreement expressly requires a rebate to decrease the latter’s fleet, if that were to happen. According to Planespotters.net, of the eight aircraft currently operated by the Express unit, two have been transferred from the mainline carrier. These two specific airframes had already been transferred to the former in 2019, but returned on the onset of the pandemic.

The other six 737, in turn, are new additions to the group’s fleet. These may be considered a replacement to the Embraer fleet, as Air Europa Express has not gotten yet to the same number of aircraft it had prior to the pandemic. Another two, also from outside the group, are expected to join the fleet shortly.

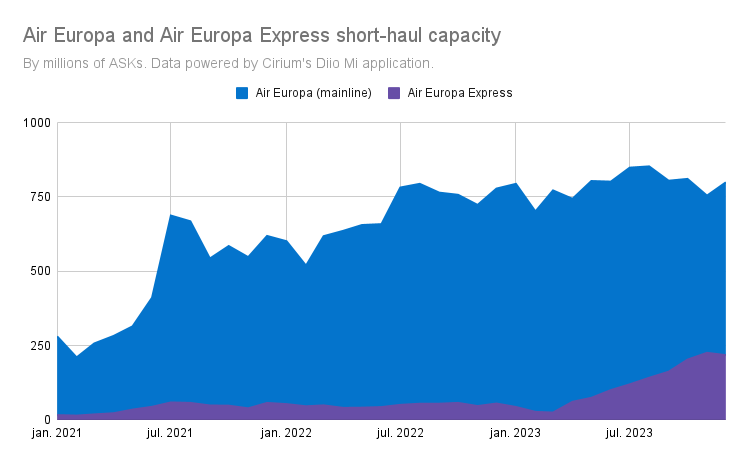

This exchange from the smaller ATR and Embraer to a larger aircraft has had a significant effect in the share of capacity each of the two airlines has. The chart below depicts that, over the last year, the proportion of ASKs produced by the lower-cost business unit has grown significantly.

Lower labor costs or not, this transition from a regional jet or a turboprop points to a clear preference of Air Europa towards not only fleet simplification, but also lower unit costs. While smaller aircraft may be easier to fill (in principle, as it has less seats), a larger one can drive unit costs down.

This is of particular importance in Air Europa’s case, as its main base in Madrid is significantly slot-constrained. By replacing the Embraer, Air Europa reveals that it would rather have a larger aircraft utilizing these valuable slots.

The fact that the group is using the lower-cost business unit, given the lower labor costs, would then be a consequence of that: it is upgauging at the lowest possible cost. Such a movement is only possible up to the limit set by the collective agreement of 18 aircraft. Air Europa, moreover, cannot indefinitely grow its presence in Madrid, given the slot restrictions.

A third restriction set to limit the Express operation (and again, assuming the new collective agreement has not given any concessions in this regard) is that the number of flight hours operated by the unit can never exceed 25% of the total flown by the group in its own aircraft.

Another question outright, and one that is more difficult to answer with the available data, is whether the airline will be able to sell these additional seats. But intuitively, with the lower unit costs Air Europa can pass these added efficiencies on to lower fares. That, in theory, would stimulate demand, all else equal.

In the routes segment, it is not clear on what types of connections Air Europe is prioritizing when adding «Express» capacity. There are both domestic routes with no low-cost competition, as there are international routes with heavy low-cost presence where Air Europa Express is the predominant carrier of the two. It is thus difficult to identify a pattern.

One possible theory — and note that is still only a guess — is that Air Europa adds Express aircraft in routes that may be weaker or under more pressure, be it from competition or from weaker demand pressuring margins down.

As an example, all major airports in Continental Europe to the west of Spain are served by mainline Air Europa, with two exceptions: Brussels and Rome/Fiumicino. Both cities see competition with Ryanair (the Irish low-cost serves Brussels through its base in Charleroi).

On the other hand, this could be disproven in the route to Milan/Malpensa: Ryanair serves Madrid not only from the aforementioned airport, but also from Bergamo. Perhaps this route can stand on its own without the help of the lower-cost unit.

Going forward, Air Europa is expected to add the first Boeing 737 MAX 8 to its fleet by the next Summer, Aeroroutes recently reported. That could open space for Express to add the older-generation 737s phased-out by the main airline.

While recovery in terms of seats and ASKs (particularly given to the upgauge from the regional aircraft to the 737), the group is still lagging behind versus pre-pandemic capacity in terms of departures. According to Cirium’s Diio Mi application, this figure stands 29.3% below in the fourth quarter of 2023, compared to the same period in 2019.

There is thus space for both Air Europa and Air Europa Express expand, at least in terms of returning to 2019 flying levels — and until the latter reaches the 18 aircraft limit, provided that the terms of the mainline pilots’ collective agreement have not changed.

As Spanish newspaper El Confidencial reported last week, the European Commission is not expected to arrive to a conclusion with respect to IAG’s takeover of Air Europa until late 2024, in the «best case scenario». As such, Globalia, the group that controls Air Europa, still has space — and time — to improve its company’s operation and margins.

Para comentar, debés estar registradoPor favor, iniciá sesión