Air Cargo Continued to Grow in October, but Trump’s Arrival Sparks «Some Caution» for 2025

/https://aviacionlinecdn.eleco.com.ar/media/2022/05/Miami-Carga-Aerea-generica-cargo-Estados-unidos.jpg)

Global air cargo demand continued its upward trend in October 2024, increasing by 9.8% compared to the same month last year. This marks the 15th consecutive month of growth in the sector, according to data released by the International Air Transport Association (IATA).

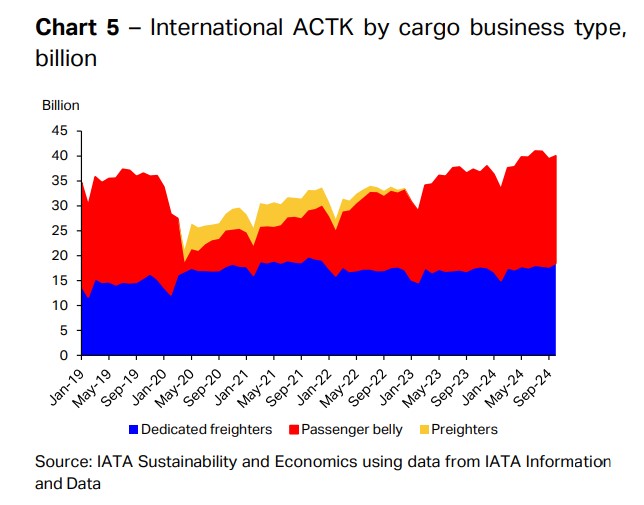

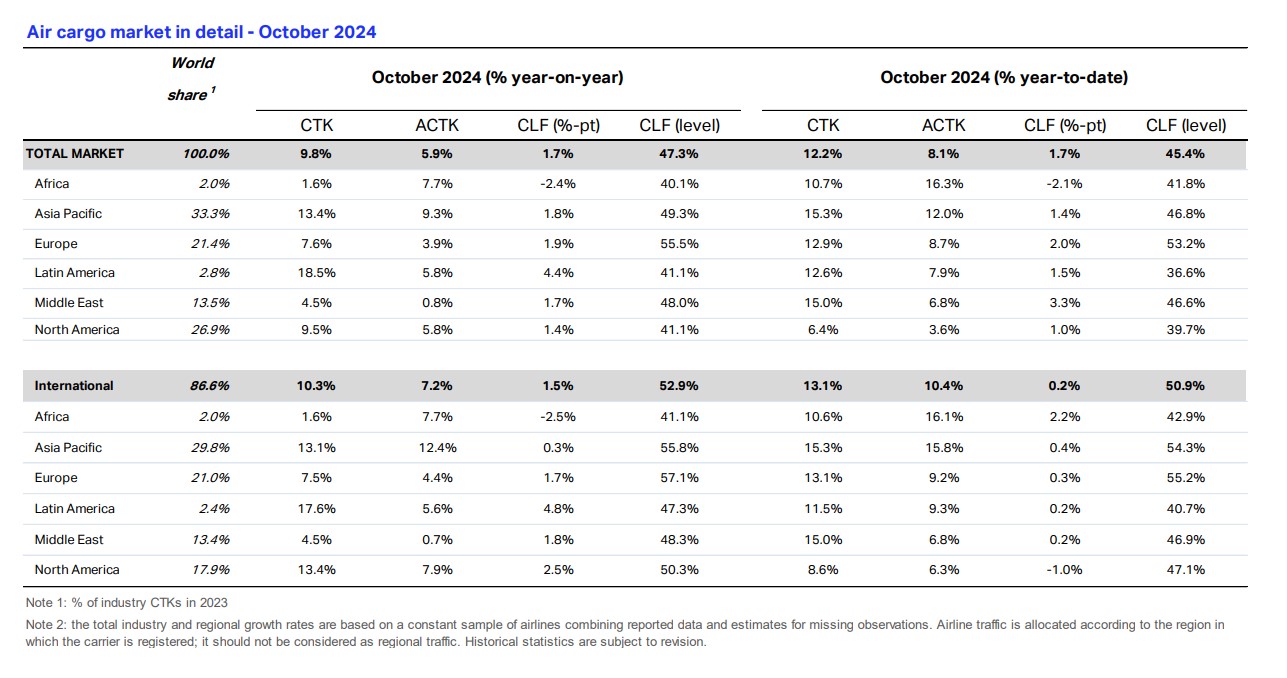

Total demand, measured in cargo tonne-kilometers (CTKs), rose by 10.3% in international operations, while capacity, measured in available cargo tonne-kilometers (ACTKs), increased by 5.9% compared to October 2023. The growth in capacity was largely driven by an 8.5% rise in international bellyhold capacity, while dedicated freighter capacity increased by 5.6%, marking the seventh consecutive month of growth, with volumes approaching 2021 peak levels.

IATA’s Director General, Willie Walsh, stated, “Air cargo markets continued their strong performance in October, with demand rising 9.8% year-on-year and capacity up 5.9%. Global air cargo yields, including surcharges, continue to rise, up 10.6% on 2023 and 49% above 2019 levels.”

«While 2024 is shaping up to be a banner year for air cargo, we must look to 2025 with some caution. The incoming Trump Administration’s announced intention to impose significant tariffs on its top trading partners—Canada, China and Mexico—has the potential to upend global supply chains and undermine consumer confidence. The air cargo industry’s proven adaptability to rapidly evolving geopolitical and economic situations is likely to be tested as the Trump agenda unfolds,» he added.

Key Factors in the Operating Environment

Several factors contribute to the demand growth. In September, global industrial production increased by 1.6%, while global goods trade grew by 2.4%, marking the sixth consecutive month of expansion. This rise in trade is partly due to businesses stockpiling inventories ahead of potential disruptions, such as the ongoing U.S. port strike.

Despite these positive trends, some indicators suggest uncertainty. The global manufacturing Purchasing Managers Index (PMI) was above the 50-mark, indicating growth, but the PMI for new export orders remained below 50, signaling ongoing weakness in global trade. Additionally, inflation in the U.S. and the EU showed slight increases in October, raising concerns about consumer purchasing power and economic dynamics.

Regional Air Cargo Performance in October

Regionally, Latin American carriers saw the highest growth, with a 18.5% increase in year-on-year demand. Capacity in the region grew by 5.8%, reflecting solid market expansion. In contrast, African airlines recorded the slowest growth, with a 1.6% increase in demand, although their capacity rose by 7.7%.

Asia-Pacific airlines led the growth in terms of cargo volume, with a 13.4% increase in year-on-year demand. Capacity in the region grew by 9.3%, further contributing to the overall market expansion. North American and European airlines also saw demand increases of 9.5% and 7.6%, respectively, with moderate capacity increases of 5.8% and 3.9%.

Performance on International Routes

On international routes, several major trade lanes continued to experience exceptional traffic levels. The Asia-North America route grew by 8.6% in October, while Europe-Asia saw a 14.3% increase, with both routes experiencing consecutive months of growth. Other notable routes included Middle East-Europe (+15.3%) and Middle East-Asia (+9%).

Airlines continue to benefit from rising e-commerce demand in the U.S. and Europe, while ongoing capacity limitations in ocean shipping favor air transport.

Download: IATA Air Cargo Market Analysis – October 2024

Para comentar, debés estar registradoPor favor, iniciá sesión